Budget 2020 has ushered in an important change in

terms of income tax

regimes. This time, there is a new tax regime that will coexist with the old one. The aim is to

simplify the income tax

regime and offer a great deal of flexibility to taxpayers at an individual

level. In that sense, the Budget has ensured that the individual taxpayer gets

a certain amount of control and choice.

Opinion

is divided on whether this new income tax regime is simplified or has turned out to be

complicated.

So, what exactly is the dual

tax regime?

One

of them is the existing income tax regime and the other one is the new tax regime. The

latter does away with exemptions;

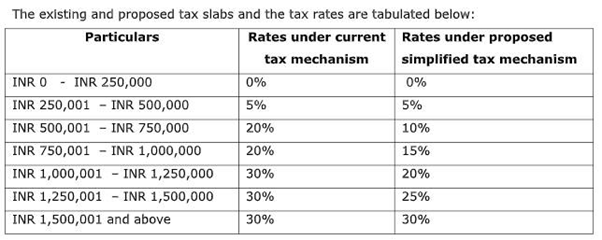

70 of them will be gone. As part of the new tax slabs, those in the Rs 5 to Rs

7.5 lakh will need to pay a 10 percent tax as opposed to the old/existing

regime wherein they had to pay 20 percent. The other slab that one should take

note of is the Rs 10 to 12.5 lakh bracket where the existing tax rate is 30 percent

while the new tax regime reduces that to 20 percent. In the Rs 12.5 to 15 lakh

category, the existing/old tax regime has a tax rate of 30 percent while the

new tax rate stands at 25 percent. The new tax regime, thus, lowers taxes.

(Source: Financial Express*)

Cases where tax rates are the

same

In

the above Rs 15 lakh category, both existing and new tax rates are the same at

30 percent. Also, under Rs. 2.5-lakh category qualifies for an exemption of

income tax under both the tax regimes. The Rs 2.5 to 5 lakh bracket is eligible

for a 5 percent tax rate under both the existing and new regimes.

The question of exemptions

If

you were to opt for the new regime, as many as 70 exemptions including standard deduction, house

rent allowance (HRA), leave travel allowance (LTA), medical insurance premium

and life insurance premium, among others have been removed. If you are someone

claiming or wishing to claim these deductions, then the old income tax regime is the

one for you. The new tax

regime is suited for those with not many investments. You can then opt

for the new scheme.

The

existing/older tax regime, which offers a wide range of tax benefits in the

form of exemptions,

incentivizes savings.

Simplification in the new tax regime

The

element of tax simplification is inherent in the new income tax regime. You don’t have to bother

about complicated filing procedures. It saves you hassles and also lowers or

removes the possibilities of errors in filing. In that sense, the Budget has indeed

simplified the tax regime. The absence of exemptions such as LTA and HRA makes

tax filing more streamlined and straightforward.

The

idea of offering taxpayers to switch to one of the two schemes every year lends

flexibility and greater choice, which is also an advantage.

The complicated element

The

simplified new tax regime

only comes into play after an individual decides on which tax regime to pick.

But to arrive at that decision, an individual taxpayer may have to make

calculations, check his/her investment profile, and then take a call. The

complication lies in the decision-making; ie, which tax regime to pick for a

year. The average taxpayer may need professional help to arrive at the

decision.

Key takeaways

In

conclusion, the system of dual tax regimes announced in the Budget is both simple and

complicated at the same time. The simplicity lies in the ease of the new tax

regime filing process and the idea of flexibility and choice for the individual

tax-payer. A tax-payer will have to choose one of them for a specific

assessment year and can switch to the older regime in the next year or

vice-versa, depending on what is more advantageous. This puts the control in

the hands of the individual. The complexity may lie in the fact that the individual

has to compute what’s the best option and then choose one of the two regimes.

If you are looking to take home loans or opt for life insurance, you may have to understand the differences in terms of tax benefits under the two regimes. Explore Tata Capital home loans or insurance schemes and decide which IT tax regime you want to pick for this year, based on the financial product of your choice.

4 mins read

4 mins read