A few years ago, a survey conducted by Deloitte mentioned that India had the second-most complex taxation systems in the Asia-Pacific region, second only to China. Now in 2020, when taxpayers were expecting simplification in the process, the recent Budget, rather than simplifying the income tax structure, made things more complicated for taxpayers.

By proposing an alternate tax structure, Budget 2020 dashed the

hopes of taxpayers expecting

lower tax slabs, increased exemptions and simplicity in the filing of

income tax returns. Now taxpayers have two paths to choose causing a lot of

dilemma and confusion. According to the new income tax structure, taxpayers can

either forego all types of exemptions and deductions entirely to enjoy a lower

tax structure or avail exemptions and deduction while paying the previous tax

rate, which is quite high.

The constant revisions in the tax system and the latest changes

in the income tax structure after Budget 2020 have added to the complexity of

our income tax system. This highlights the need for wealth management services,

as you need to realign your investment

plans and optimize tax savings and wealth creation. A wealth manager will

also help you understand whether you should continue investing in tax saving mutual funds

and other tax saving

schemes.

Additional Read:- How Can Wealth Management Help

You Save on Tax?

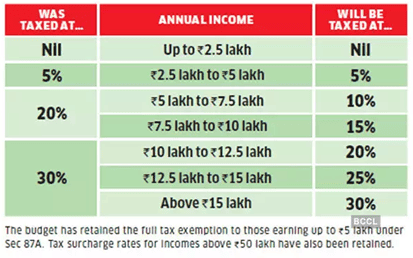

Old

& New Tax Slabs & Rates

Source: Economictimes.indiatimes.com

Choosing between the new and

old tax regime

Indian taxpayers are now left with an enormous task before filing

their income tax return in July this year. For the sake of simplicity, they can forego

all the deductions and exemptions and opt for a lower tax rate, but what about

all the tax benefits they have been deriving from their investment plans until 2019.

Suddenly, all the money that they have invested in tax saving schemes, tax saving mutual funds such as ELSS, life insurance plans

and ULIPs are not eligible for deductions and exemptions if they go for the new

income tax structure. While the new income tax structure may suit those with

minimum tax saving investments, it may not be favourable for those who have

invested in various tax saving schemes.

Tax planning post Budget 2020 has certainly become more complex

and it highlights the need for wealth management services. Tata Capital Wealth, with

a legacy of Tata’s trust among customers, specialises in bespoke investment,

protection and financing solutions that are designed according to your

financial goals. At a time when there is economic uncertainty and tax

compliance and enforcement is getting stricter and complex, Tata Capital Wealth can

help you navigate the choppy waters with ease.

Exemptions & deductions

that are out

Under the new tax regime, you will have to forego 70 exemptions

and deductions that are available to taxpayers who prefer to stay with the old

tax structure. Here are some of the major ones that a lot of taxpayers used to

rely on:

- Standard deduction of Rs 50,000

that can be availed by salaried individuals

- House rent allowance

- Deduction on housing loan

interest paid. Up to Rs 3.5 lakh for affordable housing and Rs 2 lakh for

others

- Deductions up to Rs. 1.5 lakh

for investments under Sec 80C

- Leave travel allowance (LTA), if

part of the salary structure, can be claimed for tax exemptions every two years

- Deduction of Rs. 50,000 under

NPS contribution

As per tax planning experts, moving into the new tax regime will

entail paying more tax for most taxpayers with a taxable income of above Rs. 5

lakh. However, that needs to be looked at on a case-by-case basis and only a

professional tax planner or wealth manager can help you make the right

decision.

In face of the new tax regime, it is also important that you

review your investment

plans and investments in various tax saving schemes, including tax saving mutual funds

such as ELSS.

Again, a wealth manager can assist you in optimizing your investments and tax

benefits in view of the new income tax changes.

Do I need a wealth manager?

Professional wealth management is of vital importance in India

because of the lack of a government-sponsored social security system. You need

to save for retirement, children’s education and marriage, and to meet other

financial goals.

As the investment scene gets complex because Indians are moving away from the traditional investment avenues such as real estate, gold and fixed deposits, the role of wealth managers in optimizing investments and protecting wealth is getting even bigger. Additionally, wealth management solutions also help you maximise tax benefits and comply with various tax and legal regulations.

4 mins read

4 mins read