When you need a loan, you fill out an application form and specify a collateral in case it’s a secured loan, and then wait for your financial institution to get back to you, hoping for a positive answer. But what do they do while you wait?

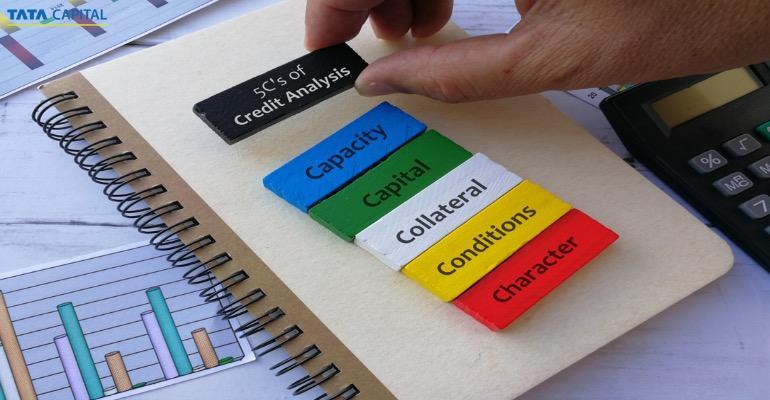

They assess your ability to repay the loan. And this is judged based on the five C’s of credit. These 5 Cs in credit are,

- Character

- Capacity

- Capital

- Collateral

- Conditions

These five Cs of credit play an essential role in determining whether your loan request will be granted. And so, here we are going to discuss these in detail, from what these five Cs of credit mean and their uses to the importance of the 5 C’s of credit. Let’s begin!

The 5 Cs of credit

The five Cs of credit are the deciding factors for your loan application. And so, by understanding what they are, you can better your chances of getting a quick loan approval by improving on the 5 C’s of credit. Let’s take a closer look at each of them.

- Character

The first C of the 5 C’s of credit is character. This criterion refers to the applicant’s overall creditworthiness. Their past credit history is a strong indicator of their ability to repay the loan. This includes past loans, credit cards and the like.

The aim is to ascertain how well they’ve managed debt in the past. The financial institution will study the applicant’s CIBIL and CRIF Highmark scores and credit reports. They check for bankruptcies, foreclosures or late payments while doing so.

The lender might even stipulate a minimum credit score for making a loan application. A high credit score translates into a lower risk of the applicant defaulting on repayment and vice versa.

- Capacity

This is a summary of the applicant’s ability to repay the loan in relation to their earnings. This requires a study of the applicant’s income, their income stability and most importantly, their debt-to-income (DTI) ratio, in case you have ongoing loans.

To calculate your DTI, all you need to do is add your monthly debt payments, divide that by your monthly income before tax deductions and multiply the result by 100.

Usually, lenders consider anything north of 43% as a negative. Most lenders prefer sanctioning loans to applicants with DTI between 28% and 36%. This varies depending on the applicant’s age and the type of credit.

- Capital

A crucial consideration for lenders is the applicant’s commitment towards the loan. The borrower’s investment in the business, including equipment and inventory, is of material value if it’s a business loan application.

Their savings, investments, capital assets, and the like are also analysed. The aim is to safeguard the lender against unexpected events in the future, such as the borrower losing their job.

Another indicator is the amount the applicant is willing to pay as a down payment. The higher the sum, the higher the chances of getting better loan conditions.

- Collateral

Collateral is what you pledge as security for repayment of a loan or credit card bills, which will be forfeited in case of default in payment. The sole purpose of security is to ensure the lender gets their money back.

Providing security might improve an applicant’s chances of getting a loan, in case their credit score is low. It acts as an added cushioning for the lender to extend the loan.

The kind of collateral differs with the type of loan. For instance, real estate property serves as collateral for mortgages, while for auto loans, it’s the car, bike, etc.

- Conditions

The last C of the five C’s of credit stands for conditions. This refers to the additional information that is pertinent to the loan application getting approved. For instance, the following information is essential to the application in case of a business loan.

- The need for additional funds.

- Proposed plan for repayment

- Health of the business; is it profitable currently? If not, why.

Apart from this, conditions of the economy, the relevant business sector, and trends in the market are also to be considered.

Importance of 5 Cs of credit

Lenders use the five Cs of credit to decide whether the applicant can be extended the loan safely. That is, whether the lender will receive their funds back under the loan terms. They help determine the risk involved in the transaction. The importance of the 5 Cs of credit lies in its ability to ascertain whether an applicant can be trusted to repay the principal and interest safely.

As for the applicant, knowing the five C’s of credit can help them improve their candidature. Let’s take a look at how.

Maintain a good credit history by making payments on time and a low credit utilisation rate.

A low DTI ratio can do wonders for your loan application. To do this, avoid applying for credit unless necessary.

A good amount as a down payment indicates your seriousness towards the loan and increases your chances of securing one.

If you take a secured loan, ensure you make payments on time and follow the terms to retain your security.

The additional conditions that influence your application may not always be in your control, but being aware of them, will help you calculate your chances of getting the loan and better prepare for its terms.

For the applicant, the importance of 5’s of credit lies in being better prepared while applying for a loan. And now, after studying each of the five Cs of credit in detail, your next loan application will seem like a breeze.

Final thoughts

The five C’s of credit play a vital role in the loan process. With these as parameters, financial institutions can ascertain the applicant’s creditworthiness and act accordingly. They also eliminate bias by putting everything in black and white. And now that you know these 5 Cs in credit, you will be applying for your next loan with a stronger understanding of the loan application process. If you’re looking for a personal loan, you’re in luck. Because we at Tata Capital offer personal loans at attractive interest rates, so you don’t need to dip into your savings just yet. With an easy loan application process and quick loan approvals, your plans never skip a beat with Tata Capital.

6 mins read

6 mins read