Floating rate funds are flexible investment vehicles. They make investments in two kinds of instruments:

A floating rate fund manages interest rate risk by changing allocation to debt instruments (buying different tenure or duration papers). It also makes use of swaps to manage the duration while choosing the optimal mix.

Unlike a fixed-rate bond, a floating-rate bond has a variable interest rate. The interest rate is tied to a benchmark rate, such as MIBOR (Mumbai Inter-Bank Offer Rate), or the repo rate, plus a quoted spread.

Say, we buy a paper with a coupon of MIBOR + 200 bps. We know that MIBOR closely tracks the operating rate (repo or reverse repo). Now, if the operating rate is hiked by 25 bps, MIBOR would shoot up by 25 bps. This means, we now have a higher coupon on our floating rate security. If we held a fixed coupon bond, the coupon would not change with a fluctuation in the rate.

AAs per SEBI’s categorization, a floating rate fund is an open-ended debt scheme predominantly investing in floating rate investments. SEBI regulations mandate a minimum investment of 65% of total assets in floating rate instruments.

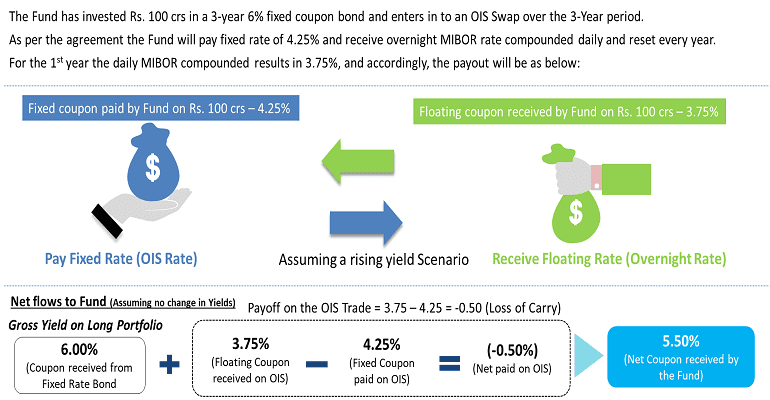

Since there aren’t many issuers of floating rate bonds in India, the market size remains relatively small. Thus, mutual funds make use of derivative instruments like Interest Rate Swaps and Overnight Index Swaps (OIS) to convert the fixed coupon yielding portfolio to floating rate portfolio.

An Overnight Index Swap (OIS) is a hedging contract between two parties, wherein they exchange or swap the interest payments on a notional principal amount. These contracts can involve a fixed or a floating rate of interest. Here, the floating leg of the swap is linked to an overnight index.

There is no cost involved while entering in an OIS contract. It has a notional contract value on which one party agrees to pay a fixed rate (OIS rate) and other party agrees to pay a floating rate (Overnight MIBOR rates daily compounded).

At the end of the periodic reset period, the net interest rate differential is exchanged with the net loss position, which pays the net gain position.

For e.g., if the overnight MIBOR rate is greater than the fixed OIS rate, then the party that had agreed to pay a floating rate will be the net payer to the position. Similarly, if the fixed OIS rate is greater than the daily compounded MIBOR rate for the period, the floating rate receiver pays the other party.

Unlike a typical debt fund where the return is fixed, a floating rate fund provides diversification to your fixed-income portfolio at a low investment limit. It invests in different types of debt securities with variable interest rates, thereby reducing the overall portfolio risk.

Duration risk refers to the risk of loss due to an increase in interest rates when you have invested in longer duration fixed-income securities. In a rising interest rate scenario, your investment in a floating rate fund offers lower duration risk compared to longer tenure fixed-income securities.

Returns from a floating rate fund are linked to the benchmark interest rate. In an increasing interest rate environment, your investment in floating rate funds can give higher returns than other fixed-income funds. However, when the interest rates fall, your returns from the fund can be lower than those other fixed-income funds.

The open-ended nature of a floating rate fund can provide you flexibility in terms of entry and exit and the tenure of staying invested.

In a nutshell, floating rate funds display flexibility and a self-adjusting mechanism in the face of a changing interest rate environment. They leverage this flexibility to manage interest rate risk and allow investors to earn enhanced accrual returns, as compared to similar duration investment avenues.

We believe such funds are well-suited for broader upcoming rate cycles and provide a suitable alternative to other debt funds/products.

If you want to invest yet are unsure of your options, then you can check out Tata Capital Moneyfy App, which is a platform that can enable and aid you in investing.

Click the “Allow” button to receive notifications

We're constantly crafting offers and deals for you. Get delivered straight to your device through website notifications.

All you have to do is click on “Allow”.

Now keep a track on your favourite fund

Go to the watchlist page to remove a fund from the list.

No funds are added to watchlist

Add your favourate funds to watchlist to keep them handy

No funds are added to portfolio

Add your favourate funds to portfolio to keep them handy

Contact Us

Contact Us

4 mins read

4 mins read

")