The interest rate on fixed deposits, whether provided by a financial institution, a government enterprise, or a private corporation, is calculated in two ways. The first is simple interest, and the second is compound interest.

Both are calculated on only the principal investment, but both differ in their consideration of the principal amount. This leads to a difference in the return amount received by the investor at the end of their investment tenure.

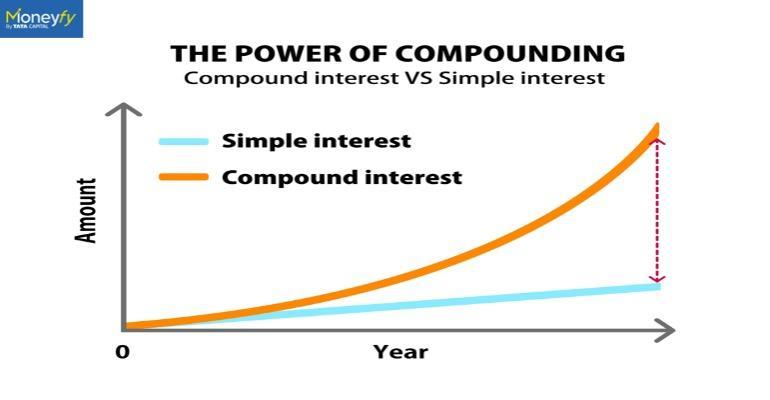

Keep reading to understand the critical differences between these two types of interest calculations.

| Compound Interest | Simple Interest |

| It is the guaranteed interest return you earn on a fixed deposit, except, here, the interest earned keeps adding to your principal amount. This, essentially, changes or increases your total principal amount. For instance, suppose you create a cumulative fixed deposit of Rs. 10,000 for 3 years at 6%, compounded annually. The first year you will receive simple interest as per the formula, which is P (Principal) x R (Rate of Interest) x T (Time or Tenure) / 100. In this case, the first year’s interest return comes out to Rs. 600. Since you are not withdrawing this interest amount, it gets reinvested, thus increasing your principal amount to Rs. 10,600. So, the second year you earn a 6% ROI on Rs. 10,600. And, on and on, it goes till your tenure is up. However, instead of using the formula above, financial institutions use the following formula to calculate the entire compound interest at the very start of your FD. P {(1+ i/100) n – 1}, where, P = Principal, i = Rate of interest and n = number of years. | It is the interest you earn on a pre-fixed principal amount over a certain period of time. Here, the interest earned is not added to your original principal amount. For example, suppose you create a non-cumulative fixed deposit of Rs. 10,000 for 3 years at 6% with a monthly interest payout. As per the simple interest formula, which is P (Principal) x R (Rate of Interest) x T (Time or Tenure) / 100, you stand to earn 10,000 x 6% x 3 = Rs. 600 in the first, second and third year. Since you withdrew the interest earned at monthly intervals, your original principal amount remains the same. However, this is only true for fixed deposits that offer monthly payouts. You can opt for quarterly or half-yearly payouts. Here, you will earn partial compound interest compared to FDs with monthly interest payouts. |

| Since the simple interest earned on the principal amount keeps getting added to the principal amount, the effective yield or the total rate of return, in this case, is relatively higher than simple interest. | The effective yield or the total rate of return, in this case, is relatively lower than compound interest. |

No one type of interest rate is better than the other. Your choice depends on whether you wish to earn a steady income from an investment or are happy keeping funds deposited for compounding.

Compare and invest in a variety of top-rated fixed deposits by logging on to the Tata Capital Moneyfy website or the Moneyfy app. Besides FDs, our user-friendly digital portal also offers seamless access to several financial instruments such as mutual funds, SIPs, etc.

To know more, visit our website today!

Click the “Allow” button to receive notifications

We're constantly crafting offers and deals for you. Get delivered straight to your device through website notifications.

All you have to do is click on “Allow”.

Now keep a track on your favourite fund

Go to the watchlist page to remove a fund from the list.

No funds are added to watchlist

Add your favourate funds to watchlist to keep them handy

No funds are added to portfolio

Add your favourate funds to portfolio to keep them handy

Contact Us

Contact Us

3 mins read

3 mins read

")